Under Armour: Why Is BOD Only Now Protecting This House?

U.S. Retail/Consumer - UAA

This is an abridged version of this note. You can find the complete deep dive note at our website here: M Squared Capital

Must admit insider purchase activity at Under Armour is extra interesting these days. Not only did all BOD members take RSU grants without selling anything for tax purposes, but also outright buying in addition to that from three key BOD members (Robert Sweeney – President Sycamore, Dawn Fitzpatrick – CEO/CIO Soros, and Mohamed El-Erian). It was the first time that Mohamed ever outright bought stock on his own, despite taking over the Chairman position from Kevin Plank. Not wanting to be left out, we recently dug much deeper into several current topics for the company including marketing efforts, product/distribution, and whether they “kitchen sinked” guidance last quarter…

There is a real brand here that resonates within North America and increasingly it seems EMEA. And now that Canada Goose, Foot Locker, Hanesbrands, Sketchers, etc. have all become M&A targets you must wonder how soon before Kevin Plank decides to vote his majority shares with a friendly in that regard…

Current guidance and consensus seem worst case scenario for both 2Q26 and FY26. We believe reasonable range for FY26 EPS is $0.05 to $0.25…

Seems Mr. Liedtke is using the same playbook that he did to turnaround Adidas where he was a key part of the Yeezy deal…

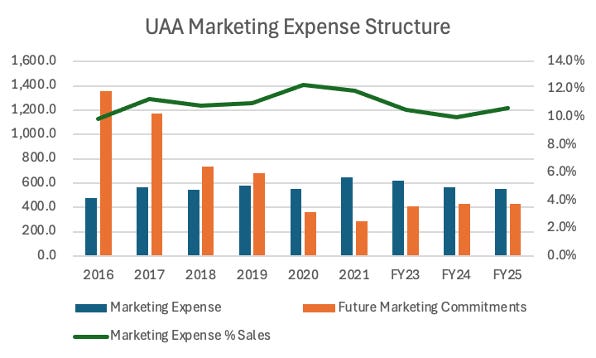

This certainly provides them with room to ramp spend on whatever trend is hottest at the moment, while peers like Nike might be less willing…

Under Armour previously said that they would be opening accounts in 2025 but primarily at boutiques. It probably would be hard for Under Armour to build a meaningful boutique business if its brand was always on sale at Nordstrom…

There is minimal, if any, presence of Under Armour product at specialty running retailers such as Fit2Run or Road Runner Sports yet we would expect this shoe to get better attention than in the past given success in the field…

However, we haven’t seen much of Halo (which launched August 7th) anywhere other than Under Armour’s own DTC channel…

Tariffs are worth about 200 bps to gross margin in 2Q26. But that should only impact the North America region. So why is it that you need to have EBIT margin pressure akin to 900 bps in that region to have a chance of getting close to their guidance?

Of course, there is the $27 million insurance benefit they got last year in 2Q25 but for some reason decided not to adjust numbers for. Yeah, they disclosed it in the 10-Q but the entire idea that they decided it wasn’t meaningful to their never-ending adjustments is comical…

Lastly, the lead up into the World Cup should be a major event for Under Armour given how strong their cleats business continues to appear…

Add your email to our list to get much more timely notifications of new research. As of now we have dedicated coverage of Deckers, Floor & Decor, Nike, Restoration Hardware, Tractor Supply, Under Armour, and VF Corp. So much more to come…and soon…

FIN