"Send In The Cleaners" Under Armour Style

U.S. Retail/Consumer - UAA, NKE, FL, DKS, KSS, ASO, M, JWN, JD Sports

All content on this substack is free.

If there was ever a time for Under Armour to get its act together, it’s when Nike is in disarray. Under Armour was on a straight trajectory to ample success until Nike became determined to kill their footwear dreams out the gate. The investor day last week (12/12) highlighted both future product and new capabilities. But none of that matters if Under Armour hasn’t cleaned up its own act first.

We thought it would be helpful to take a deep, data driven review of distribution improvements to date. Under Armour has spent the last year proactively cleaning up distribution in anticipation of a full slate of new product launches on the horizon. The key takeaway: This is already the healthiest version of Under Armour that we have seen for this entire decade.

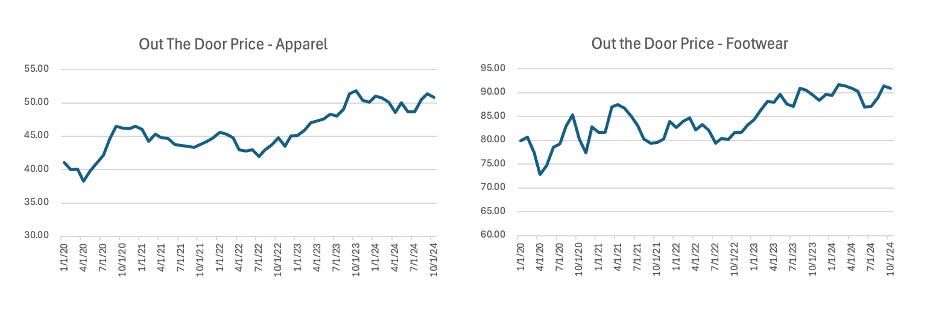

Kevin Plank recently stated “We're a brand that's earned the right to exist and that we're a premium brand.” One of the bigger investor concerns about Under Armour is that the brand may be damaged and/or lack pricing power with consumers. The data suggests that this may be an antiquated view. Under Armour has experienced a meaningful lift in initial footwear list price, particularly over the past year and half. Apparel has also increased but to a lessor degree. When combined with a general trend towards fewer markdowns in both categories over the past year, this presents a much healthier picture of how Under Armour’s product is resonating with consumers.

Under Armour Apparel & Footwear List Price vs. Markdown Mix

Source: Flywheel Alternative Data

This has all translated into the strongest levels of out the door pricing at Under Armour in both Footwear and Apparel for the past five years. We saw a little bit of weakness mid summer, which corresponds with management commentary towards taking inventory action.

Under Armour Apparel & Footwear Out The Door Pricing

Source: Flywheel Alternative Data

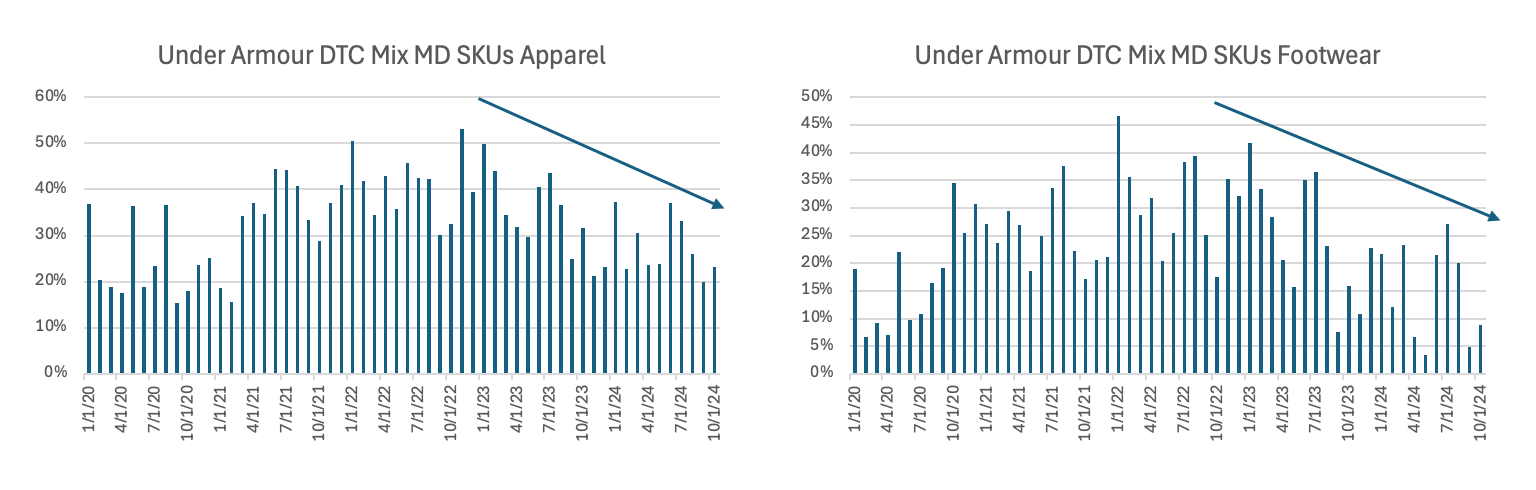

DTC

The company has taken proactive actions to reduce promotions and discounting in its DTC business, which has served as a tailwind to profitability this year. It is clear they have made solid progress towards this goal as the heightened DTC promotional levels from 2022 have largely been cut in half for both Apparel and Footwear product. If Under Armour can’t maintain its premium positioning in its own DTC channel, very hard to expect them to sell anything at a premium price point in wholesale, so we find the underlying trend encouraging.

Under Armour DTC Apparel & Footwear Mix of Markdowns SKU’s

Source: Flywheel Alternative Data

Wholesale

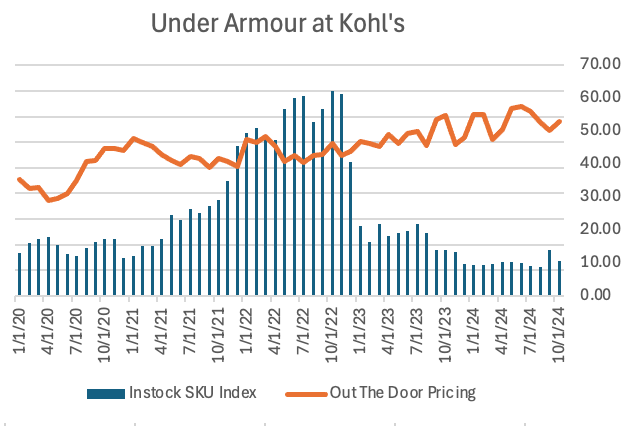

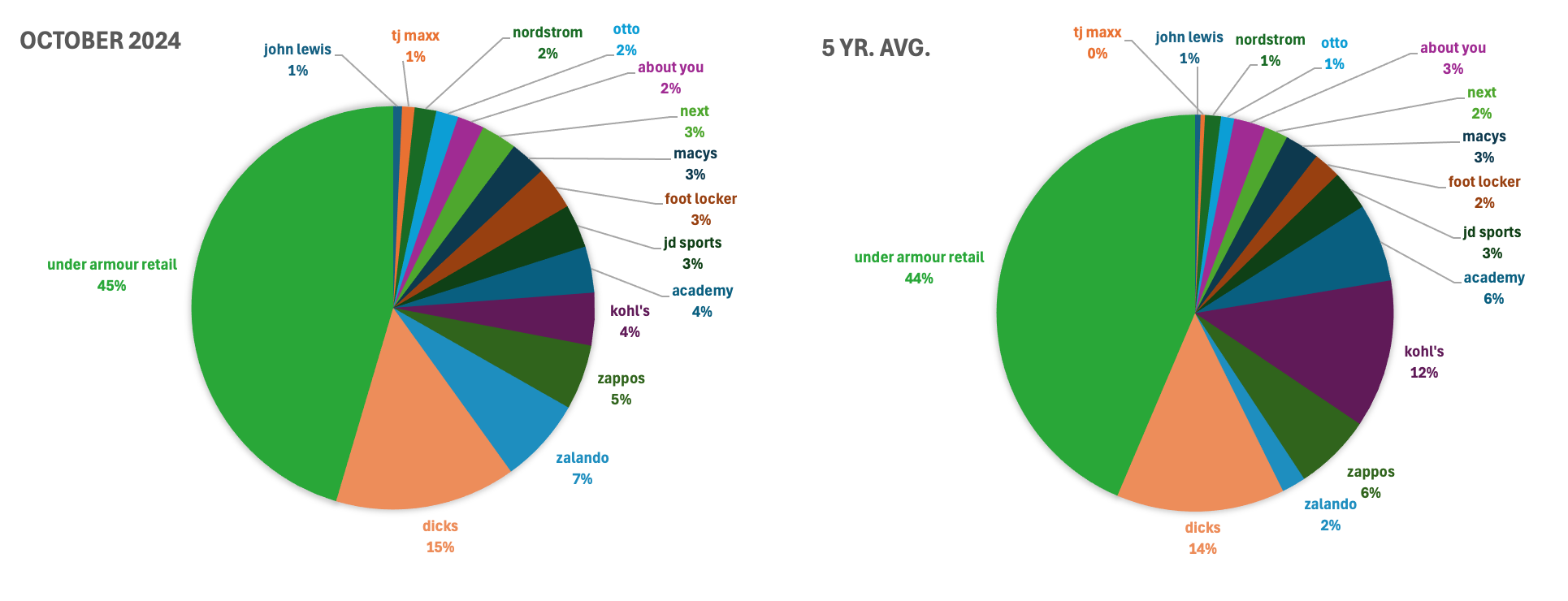

Under Armour has substantially reduced its reliance upon Kohl’s as a distribution point (as measured by total number of in-stock SKU’s). While Kohl’s remains a top five wholesale partner, its relative mix in the top 15 has decreased to 4% from a five-year average of 12%. One of the largest bear thesis’ over the years has always been how much Under Armour relies upon Kohl’s for distribution but that no longer seems as relevant.

Under Armour Top 15 Distribution Points

Source: Flywheel Alternative Data

But more importantly, they seem to have really cleaned up a lot of their remaining business at Kohl’s in their efforts to heighten the premium position of the brand. The company has dramatically reduced the number of in-stock SKU’s from the peak in 2022 but current levels remain roughly half of what they were at the beginning of the decade. Meanwhile the average price of product has increased 20-30%.

Under Armour In-Stock SKU Index at Kohl’s vs. Out The Door Pricing