RH: Time For A Resto In Hype

U.S. Retail/Consumer - Restoration Hardware (RH)

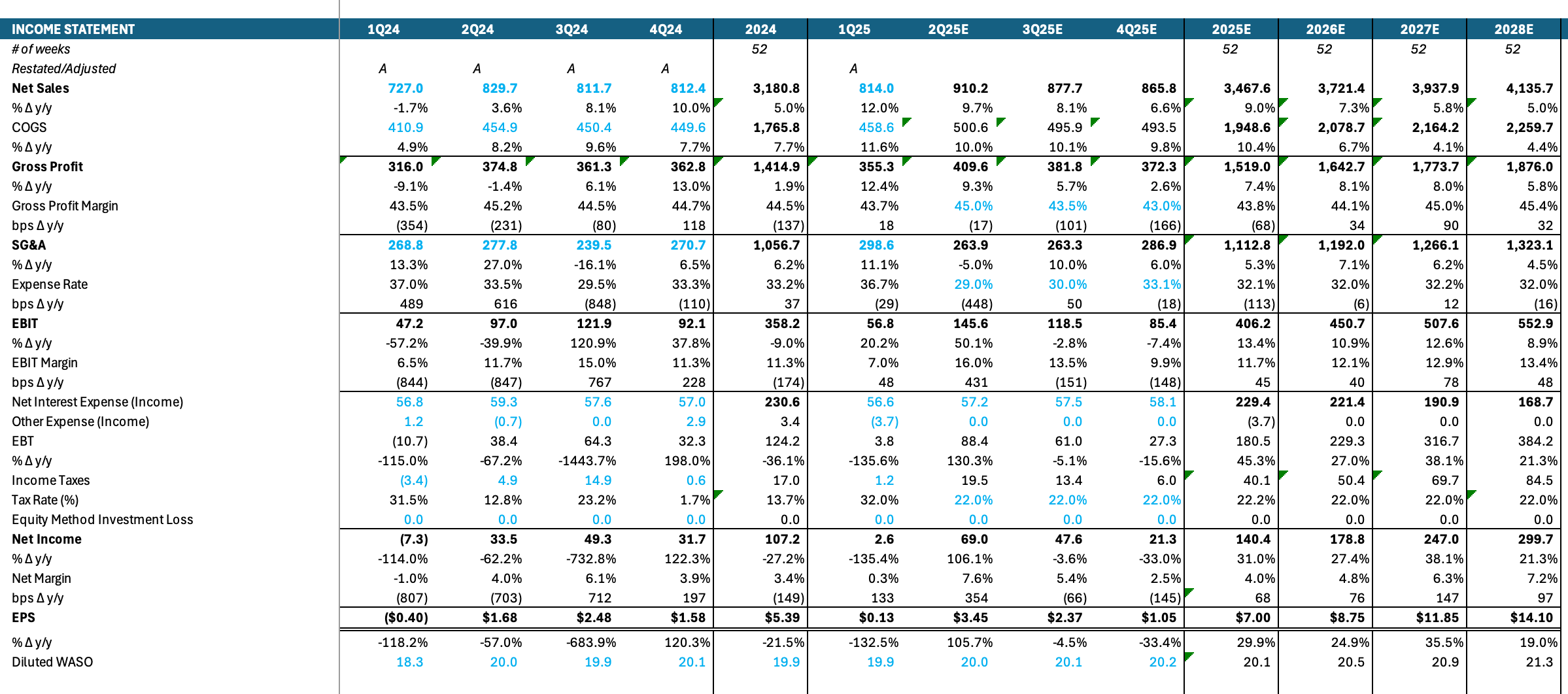

Circled back to Restoration Hardware after a few days of percolating 1Q25 results. Give quick hits on things that stand out but deep dives on international commentary and how sell side consensus numbers shook out. The net takeaway here is I am still negatively biased to the story. We maintain our $11.00 high end EPS scenario this year but decreasing the low end of the range to $7.00 from $8.00.

Restoration Hardware 1Q25 Things That Make You Go Hmmmmmm

On the positive side, customer deposits increased 10% this quarter, which was the best result in three years. However, very hard to reconcile with guidance for an expected 600 bps revenue disruption from tariffs in 2Q25. The conspiracy theorist in me thinks it’s because anyone in the market for custom furniture pulled the trigger on buying before prices increased due to tariffs. Will be interesting to see how that plays out through gross margin over coming quarters.

They only drove $18 mm in cash flow from inventory this quarter despite going to a 30% RH Member discount in mid-March. Not a good sign when Gary says they: “continue to have excess inventory of $200 to $300 mm at cost, that we plan to turn into cash over the next 12 to 18 months as we optimize our assortments post our product transformation.” I still very much wonder what this means for their manufacturing vendors as that represents about one entire quarter of product costs in COGS. Pretty sure they can’t go three months without orders.

Regarding the Outdoor discount of 35%, why would this happen if they never raised prices: “While the business started strong, we experienced a slowdown following the reciprocal tariffs”? If anything, they lowered prices because they increased the RH Member discount to 30% several weeks before Liberation Day even happened.

The reduction in capex plans for the next few years is highly difficult to jive with expectations to open 7-9 galleries per year. Gary himself said it best this quarter with: “Post- COVID the cost of building one of our galleries is almost twice as much”. Of course, right as he is running out of cash, he somehow developed a solution called the “design compound” that apparently cuts that cost in half. Gary certainly seems to have a lot of convenient things happen when he talks about the future and inconvenient things happen when he talks about the past. He hasn’t opened a single one of these yet so clearly a higher risk profile than before to say the least. Not to mention difficult to understand the scale here.

The more I think about this “design compound” concept the more warning signs arise. They haven’t even tested it yet. Gary loves to come fast and hard when he does something new and while that worked for the next generation store rollout in 2015 it was disastrous for both the original Modern rollout as well as international. Keep in mind that all his successes came during ZIRP and now there is a cost of capital. Further, he is adding the risk of an entirely new store format in the US on top of a highly concerning international situation. I wonder if this compound design reduces the mousetrap features of existing galleries. For example, can I now just walk straight through some lovely gardens to get to the restaurant without even having to look at much furniture? Guess we will find out next year with Aventura, East Bay, and Naples – if that’s when they open.

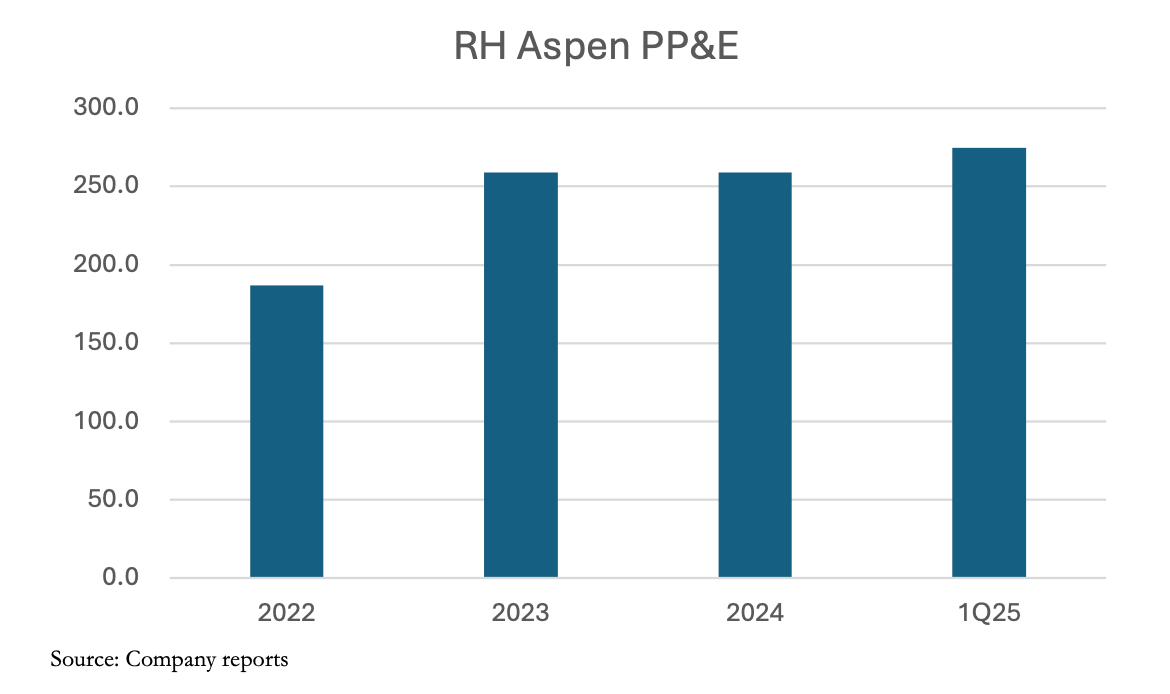

I really don’t know how Gary is coming up with this $500 mm in real estate he can sell. He said the same thing in 4Q24 and I didn’t look into it too hard but something doesn’t seem right here. Per the 10K they only own three stores that are currently operational. Everything else is related to Aspen (nothing is operational). I don’t know where he gets to six locations for sale/leaseback unless he is already including properties in Aspen. While he has spent a ton of money on Aspen much of it appears to be a boondoggle and the recent sale of a house for 2x the price paid in ~2020 is probably not the best indicator of what the rest will go for.

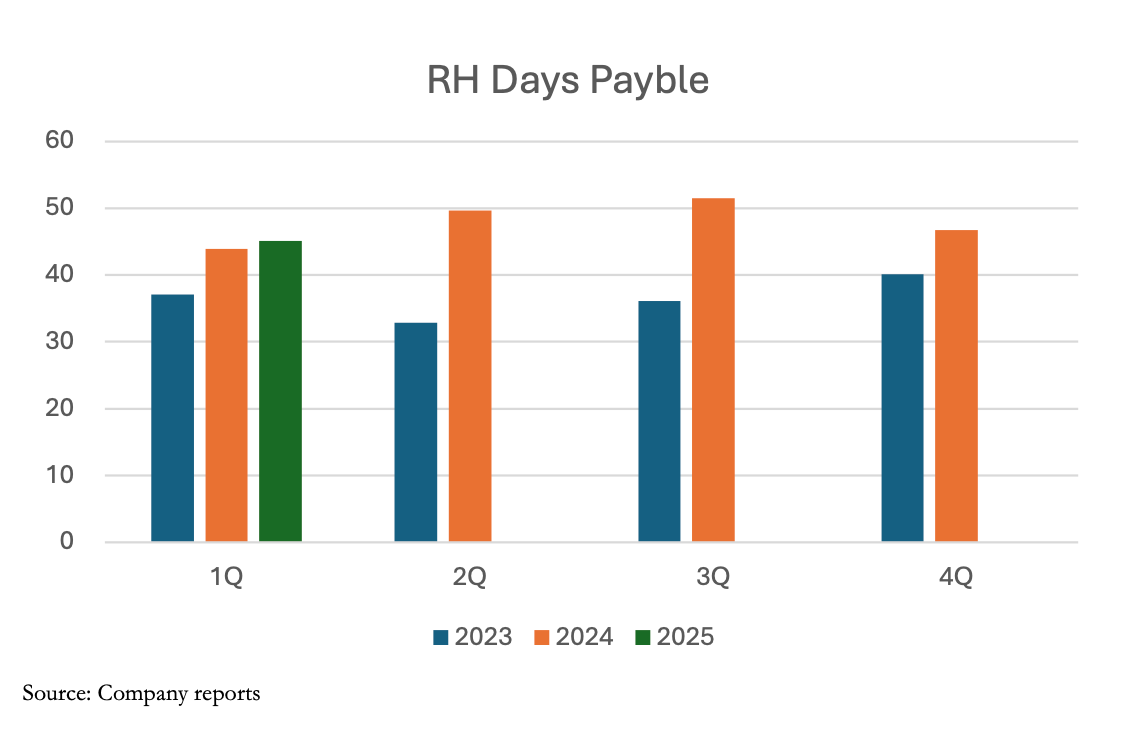

Most recent example of Gary never being straight with shareholders: Back in 3Q24 he said RH would no longer source from China by 2Q25. Mind you this was well before liberation day and retaliatory tariffs. And that’s even despite fact they sourced more from China in 2024 (23%) than 2023 (22%). Silent to the topic in 4Q24 and only now we hear they still did 16% in 1Q25 and should only get to 2% by the end of the year. You can never rely on a single thing he says. Ever. Best part is they expect a “meaningful portion of the tariff absorbed by our vendor partners” when their like for like days payable only continue to increase. I am shocked that despite running a 60% off clearance program since September 2023, increasing the RH Member discount to 30% in mid-March 2025, and introducing a RH Member discount for Outdoor of 35%, days payable only continue to increase.

RH International

We firmly disagree with renewed investor optimism towards international growth following 1Q25 earnings. If things are getting so much better, then why are they calling yet another 180 bps EBIT drag from international expansion this year (particularly as they already wrote down Germany). This is the exact midpoint of the expected drag of 160-200 bps that they called out for initial 2025 guidance during 4Q24, so certainly not better per se. This is on top of the 230 bps drag in 2024 and 150 bps drag in 2023. It makes no sense given how few stores there are and how they apparently all are ramping in productivity.

Let’s start with Germany as 60% comparable demand growth might sound great until you realize how low the base was to begin with. RH wrote these stores down and didn’t renew the lease because “assets were not recoverable on an undiscounted cash flow basis”. That implies a horrific level of revenue that even 60% growth (of course only using “demand” and not real revenue) itself probably won’t help with. More importantly, they took the write down ~11 months after opening so likely were well-aware of any trend towards improving results. There is nothing to indicate why a massive step function change magically occurred to that trend during Dec-2024 and April 2025.

RH went so far out of their way to include the Germany data point that they had to include the definition of “comparable galleries”. RH Brussels certainly meets this definition as it has been open more than 13 months (opened March 2024 and 1Q25 ended on May 3, 2025).

“Comparable Galleries represent locations that have been open for at least 12 consecutive months as of the end of the reporting period and did not change square footage by more than 20% between periods.”

Why did they not provide any color towards RH Brussels? What did they explicitly call it “non-comparable”? This store is exceptionally important to the international story because it is the closest thing to a direct read on the upcoming RH Paris. Not only is French a common language there the city has historically been a highly popular destination of wealthy French exiles for tax purposes.

Let’s switch to RH England (Aynho Park). Gallery up 47% and online up 44%. For full year 2025, they expect the gallery to reach $37-$39 million and online to reach $8 mm. The only other time they gave these numbers was 3Q24, when the gallery was running up 42% from July to December and online was up 111%. So slight acceleration in growth at gallery but massive deceleration for online. More importantly, back in 3Q24 they said the gallery and online will reach $31 mm and $7 mm respectively by the end of their second full year, which ends during the middle of 2Q25. So in the remaining 2.5 quarters of the year, they only expect to grow the combined business by $7-$9 mm. Certainly a significant slowdown in growth relative to the impressive sounding figures with no context that Gary used for 1Q25.

Now is a good time to remind everyone that Gary originally hyped RH England to do $50 mm to $250 mm. But more importantly, he explicitly said a $50 mm run-rate would be margin dilutive. This is the definition of a long-term structural barrier to margins and something bulls need to consider when blindly slapping peak EBIT margin on some future revenue figure.

I remain skeptical of RH Paris opening in September but if you throw enough money at something then magical things happen. Gary certainly has a huge incentive to get it done as the timing of Maison et Objet is probably the best possible setup for opening success in what many investors are highly skeptical of. Likely an important factor to consider when thinking about SG&A spend for 2Q25 and 3Q25.

The company hasn’t mentioned RH Sydney in a shareholder letter since 1Q24, which was in an immaterial manner. Gary last mentioned it in a similar immaterial manner during the 2Q24 call. The last time it was prominently mentioned was 4Q23 where they talked up the “five-story development” and set a Fall 2026 opening date. They used to talk about it prominently every quarter before that for several years. At one point it was even supposed to originally open in 2025. They still mention it in the SEC filings though.

Clearly most of this is just narrative management – is it any wonder these figures are in the “demand” metric most people no longer believe following 4Q24 (and that Gary himself said they wouldn’t use this year until backtracking a few days later due to the stock price). Gary finds every possible data point that can be spun positively but as always fails to provide proper context, even going so far to use stores already written off. I don’t know how many more times investors will fall for it but the substantial pullback from early strength on Friday implies his credibility has waned somewhat relative to before.

A common rebuttal I hear from bulls is: “international is doing so much better than all the negative sentiment from last year.” Well, yeah. It was almost mathematically impossible to do worse. Not sure how you can say all this wasn’t already incorporated into expectations for 80%-100% EPS growth this year.

Lastly, regarding the LT growth rate, does anybody think RH can add 7-9 galleries per year without success in international markets? The abrupt ending to discussion on Sydney coincided with this entirely “new concept” that Gary is rolling out. Probably the best indication of where the company internally sees greater returns (of course anything “new” is a lot riskier in that regard).

RH Model Thoughts After 1Q25 Guidance And The New Sellside Consensus

Main takeaway: Keeping my high end EPS scenario of $11.00 this year but taking the low end down to $7.00 from $8.00.

It seems the street has modeled leased selling square footage growth substantially better for this year. Did it have anything to do with me publicly posting my schedule of store expansion? Who knows, but many of them do follow me.

The sequential progression of comp sales for consensus is very strange as they get worse in 2Q25, better in 3Q25, and worse again in 4Q25. Granted the compare is more difficult in 4Q25 but it is somewhat difficult to understand the optimism behind strength in 3Q25. Tariff pressures should remain and the benefit to furniture from any potential rate cut is likely to have a lag.

Street has roughly 90-100 bps of gross margin expansion each quarter for the rest of the year. I simply don’t know how you can possibly have meaningful positive gross margin either in 2Q25 or for the rest of the year. The new 30% RH Member discount is permanent and they made practically no progress on clearance inventory. In particular they are likely to have greater occupancy pressure in 2Q25 relative to 1Q25 given the 600 bps tariff headwind to sales and product margin also includes the temporary 35% RH Member discount for Outdoor product. The impact of tariffs is likely to begin flowing through 2H25 COGS and there should be significant occupancy pressure in 2H25 from all the new stores they are opening. You have to assume international ramps up quickly but the company continues to call out 180 bps of EBIT pressure there for the entire year.

The SG&A rate for the rest of the year is equally questionable. The street is modeling it down 0.5% in 2Q25 but that’s up against 27.0% growth in 2Q24 when they had probably the largest Source Book mailing in company history. A more relevant comparison for what 2Q25 could look like is the 16.1% decline in 3Q24, which was up against a similarly large Source Book mailing in 3Q23. Lastly, I am perplexed by the street only growing SG&A dollars by 1-3% in 2H25 when the company has its largest concentration of store openings this decade.

I understand why the street modeled this way in aggregate as they were trying to align with RH’s EBIT guidance. Right now they are around the midpoint of the 15.0-16.0% EBIT guide for 2Q25 and low end of the 14.0-15.0% EBIT guide for full year 2025. Gets you to roughly $10.50 in EPS. I think if RH gets anywhere near its margin guidance the consistency of gross margin to SG&A will be significantly different than how the street is modeling though.

Personally, I am incrementally more negative based off the model. I had them crushing earnings in 1Q25 at $0.20 on even my downside scenario but all they could do is $0.13. What scares me most is all the advertising expense that flowed through 1Q25 should help 2Q25 revenue in a big way but alternative data already says it isn’t, not to mention the massive 600 bps callout to 2Q25 revenue from “tariff” related issues. Not sure how they make any of this up in 2H25, other than square footage expansion. TBC, that is super low quality for total revenue growth or EPS, particularly given inflationary costs towards any new stores. I think Gary was proactively trying to manage this narrative during the call by saying he was looking at an entirely new format for growth that magically is half the cost.

Am going to keep the high end of my EPS range at $11.00 but lowering the low end to $7.00 at this moment. I continue to think current visibility favors the downside so am posting a picture of my income statement in that scenario. You can download the model I have used since 2015 for free and plug in whatever assumptions you want. I will always provide my RH model for free on my website, which is www.msquaredcapital.com.

FIN