RH 1Q25 Preview: Sometimes The Discount Becomes Permanent

U.S. Retail/Consumer - Restoration Hardware (RH)

All content on this substack is free.

It’s my favorite time of year as Restoration Hardware is set to report 1Q25 earnings this Thursday. Sentiment has shifted negative but never count Gary Friedman out! He certainly has reasons to stick it to Wall Street now that his corporate grifting is increasingly exposed. As always, we provide detailed thoughts:

Key Takeaways For 1Q25 Preview

I have previously mentioned that sale activity is likely the canary in a coal mine towards liquidity issues. The recent acceleration to all time high levels, combined with an ever increasing RH Member discount, should be concerning to all. I presume that Gary originally planned to increase prices this year as he made headway on clearance inventory but now it appears that whatever related margin benefit is probably lower. Wouldn’t be shocking that Gary misjudged the underlying elasticity of his product.

Liquidity needs are ramping too because most capital projects this year are slated for 2H25. This is a big year for new store openings, not to mention the launch of entirely new concepts. While some of that capex has already flowed through, I would assume peak needs are likely sometime now to the end of Summer for most of these stores.

I want to say that it’s hard to see any issues with 1Q25 itself given how far into the quarter they gave guidance. April 2025 was the first time we saw a y/y decrease in promo emails dating all the way back to when they started in September 2023. Gary sounded like he sandbagged the quarter when he spoke on CNBC and even his wife posted on Instagram the phrase “I wouldn’t bet against him”. Can only imagine the strings he would pull to ensure a happy marriage.

However, trends appear to have got significantly worse at some point. I hear recent credit card data is not good. Clearly the massive acceleration in promo emails in May points to something changing. One explanation for the stealth 30% discount was that it was always meant to be temporary but now they are making it explicit for some reason. Once you do something like that, it’s hard to lower it in the future.

Positioning into this print is very difficult as a solid beat on the quarter combined with a guide-down for “tariff” reasons might actually clear the deck for investors to once again get involved. Gary seems to have levers to pull in 1H25 for EPS but it gets much more difficult afterwards. Also remember that Gary can and will say anything so is a major wildcard, although he lost a lot of credibility last quarter. Right now my range of EPS outcomes for the year is $8.00-$11.00, with greater visibility to downside than upside.

I am uninvolved right now. Probably will just stay entirely away from it and play whatever swing happens afterwards. Although I am tempted to put a small bet on downside tail risk just so I can be there if story breaks (low probability). Let’s see what the market gives me this week.

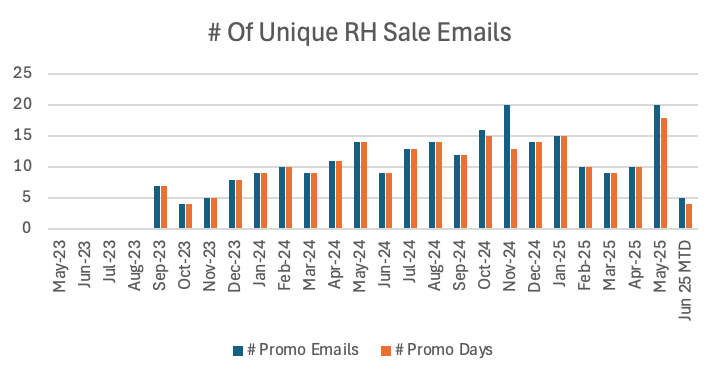

Promo Emails - 1Q25

The main takeaway here is that RH is currently more promotional than ever, if that was even possible.

A curious thing happened on May 16th: RH decided to increase the RH Member discount to 35% on Outdoor product “for a limited time”. This follows the company doing a stealth increase to the RH Member discount for all products to 30% (vs. 25% before) on March 10th. This was “stealth” because all email headers continued to promote the old 25% rate all the way up until yesterday, when they finally updated them to 30%. Previously you had to scroll down to the bottom of the email to see the new 30% rate.

Not sure how Gary benefitted from hiding the new 30% rate in email communication. Makes you wonder if this was simply incompetence rather than strategy.

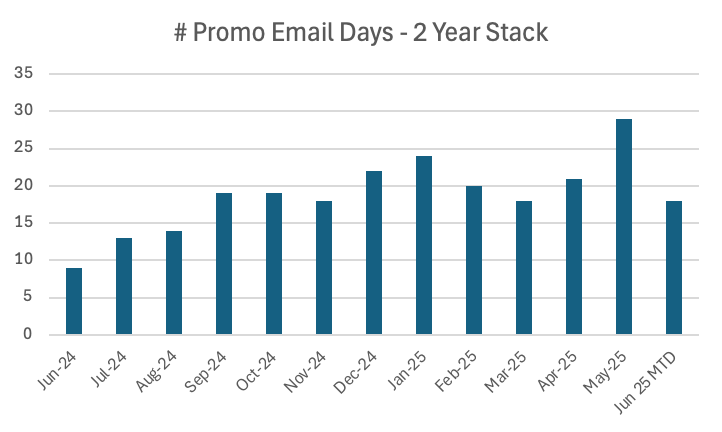

May was tied as the worst month for total number of sale emails with November. However, it was by far the worst month for total number of sale email days, coming in at an astonishing 18 days vs. prior peak of 15 days. Its not perfect but I like to look at the two year stack for this metric to gain a sense of the overall trend. May was a massive acceleration of sale email activity on top of what was a very busy May in the prior year, leading to a new all time high in the chart.

I specifically exclude RH Outlet emails from this analysis but can tell you that channel was also extra active during May (as well as all year long, which is very different from history).

This morning we got an email that says the 35% RH Member discount for Outdoor product ends tomorrow. Just in time for the earnings call! I wonder if it starts back up next weekend. The never-ending coincidences with this story are quite comical. Its almost like Gary spends more time managing the narrative than the business…

Web Discounting - 1Q25

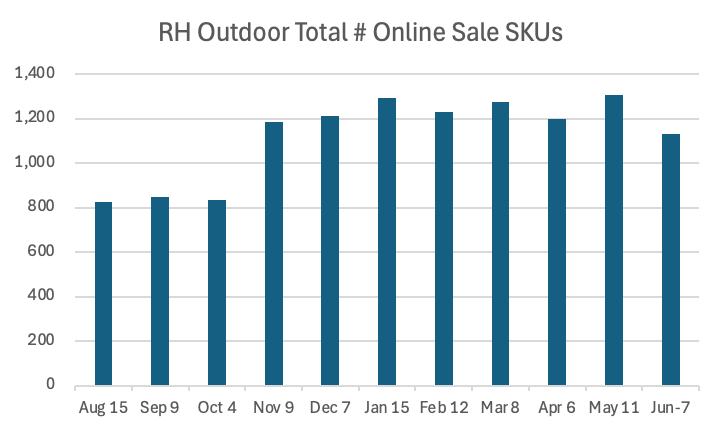

Let’s see how much progress Restoration Hardware has made clearing inventory online YTD. Looking at the five largest categories we see that only one, Outdoor, has fewer SKU’s in the website clearance section than at the beginning of the year. More on that in a minute. Clearance for the other four categories has substantially increased. Mind you, this is after a massive increase in clearance SKU’s for all of these categories last year.

Regarding the improvement in Outdoor, funny how most progress was made immediately after they ran the new RH Member discount for Outdoor. Just prior to that date Outdoor clearance SKU’s sat at an all time high. It's possible they were able to clear some of that inventory. Or, I suspect more likely, they simply transitioned some of the clearance product back to full price selling in hopes to get a better out the door price. It's simply just too difficult to tell at this moment.

Price Increases - 1Q25

There is a lot of chatter that RH apparently raised prices a month or so ago. Can you blame them when 23% of their product was sourced from China last year? Apparently, one of the channel check providers like Cleveland or somebody else was saying this. Last year I also heard second hand that Gary mentioned in meetings they were planning on raising prices at some point during this year.

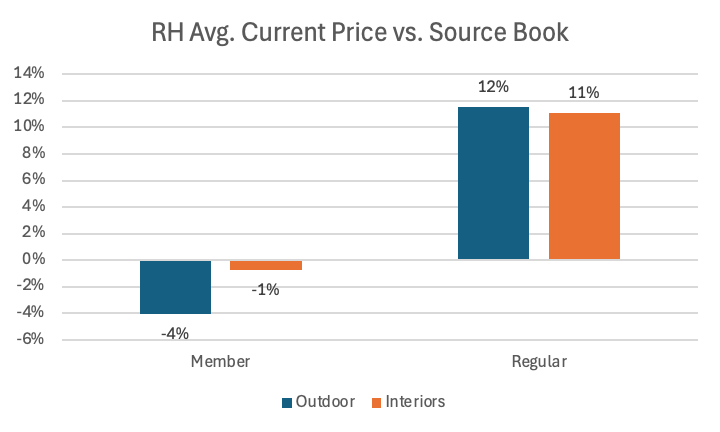

This shouldn’t be too hard to check. I have hard copies of all the Source Books. Did price spot checks for all items on 10 random pages of the most recent RH Outdoors and RH Interiors books.

We looked at 24 total items in Outdoors, of which 21 currently have a lower RH Member price on the website than the Source Book. However, only three items have a lower Regular price on the website than the Source Book. For Outdoors, the average discount for RH Members was -4%. The average premium for Regular was 12%.

We looked at 32 total items in Interiors, of which 15 have a lower RH Member price on the website than the Source Book. Only two items had a lower Regular price. For Interiors, The average discount for RH Members was -1%. The average premium for Regular was 11%.

Now is a good time to remind everyone that 98% of RH’s sales are through its Member program, so Regular pricing is irrelevant. Effectively whatever price increases the company took to offset tariffs are being more than offset by the new 30% (35% for Outdoor) Member discount.

Model Forecasting Thoughts - 1Q25

It certainly looks like he sandbagged 1Q25. Hard for me to understand what he is ramping so much SG&A on during this specific quarter to limit the upper end of the EBIT guidance range to 7.0%.

I have a hard time with gross margin for the full year. After last quarter I had them with modest gross margin expansion, as it felt like we hit a trough in product margin and the productivity (occupancy) drag from new stores later this year is offset by ramping productivity in stores opened last few years.

Now that we have seen incremental member discounts that seem to more than offset any price increase benefit, as well as a massive ramp in promo activity, I think its prudent to expect yet another year of gross margin pressure in 2025, albeit more modest than last few years.

Gary has a lot of room to cut SG&A in the front half though to offset much of this pressure and still deliver on earnings. He can probably cut $50 mm out of advertising alone in 1H25. Its going to get a lot more difficult for him in 2H25 though given all those new store openings. In particular, 3Q25 should look really bad given the compare against 3Q24 when they cut $46 mm in advertising vs. the prior year.

Without gross margin expansion I can easily get to a full year EPS number around $8.00, particularly if I assume comp store sales peak in 1Q25 and sequentially decelerate from there. And that’s still assuming a very healthy full year comp. Let’s call that the low end bound for the potential range of outcomes. Right now I think you really can’t expect more than the ~$11.00 the street was expecting immediately post 4Q24 results as the high end, given recent developments, and that’s even assuming they put up a solid beat in 1Q25.

FIN