On Holding: Good Story But Just Doesn’t Turn Us On

U.S. Retail/Consumer - ONON

This is a highly abridged version of this 9 page note. Subscribers can find the complete deep dive note and financial model at our website here: M Squared Capital.

We sized up the ample promotional activity for On Holding across most of the wholesale channel and while we are not worried about the near-term, warning signs are starting to flash. Therefore, we also took a much deeper look at what appears to be a positive inflection towards accelerating growth for the China business which is likely the company’s prime lever to offset any decelerating growth in Western markets. We also investigated the nascent apparel business to see if there was any chance of that becoming a meaningful growth opportunity anytime soon to take the broader company to the next level. Some of the U.S. pressure likely comes from an ongoing transition to newer product models and investors recently witnessed how a story like that can ultimately play out with Deckers over the past year, which we explored the similarities. The simple fact is On is now bumping up against that mythical $3 billion in sales barrier that has been troublesome for most athletic brands in history to break through without meaningful resistance. We think they will have no problem surpassing that level (especially when considering inflation) but the idea they will sustain amazing growth rates into the next mythical barrier of $5 billion in sales seems aggressive. In the history of mankind, there have only been six athletic brands to meaningfully surpass that amount: Nike, Adidas, Puma, Lululemon, Under Armour, and New Balance (not using GMV). None of them did it easily…

Of major franchises that the company often discusses, we noticed several of the latest iterations amongst the sale SKU’s at Nordstrom, including the Cloudnova 2, Cloud Runner 2, Cloud Tilt, Roger Advantage Pro, and Cloud X v4…

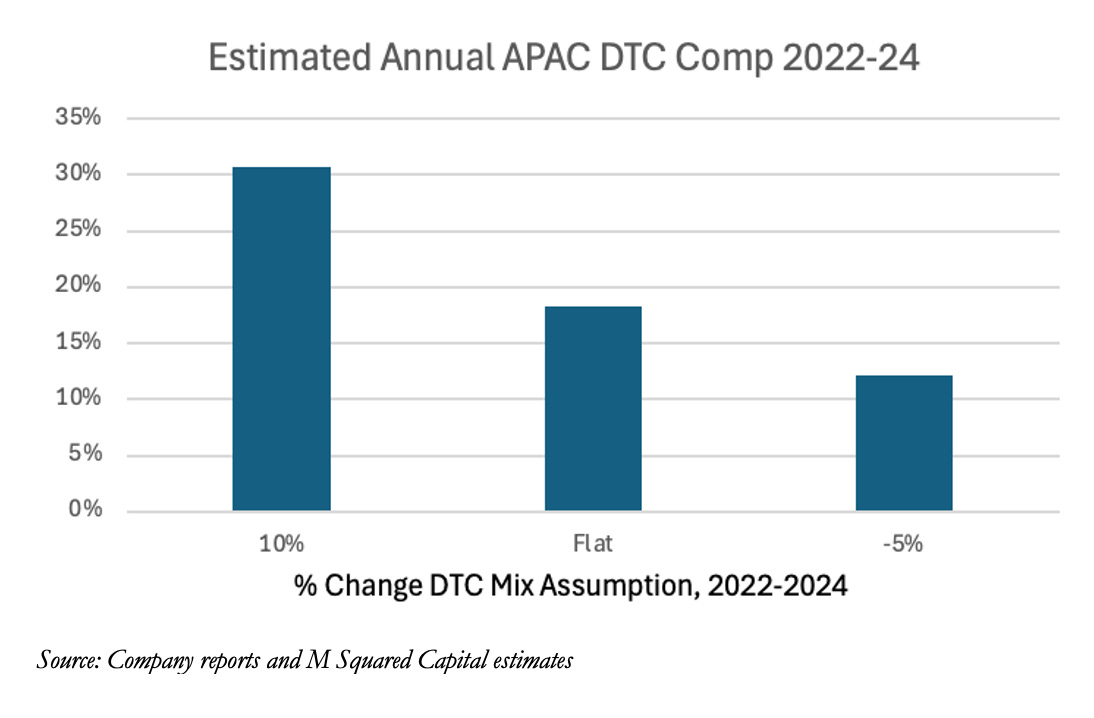

Over the past two years we estimate that total DTC sales per store productivity is up 40% for the entire APAC region (largely China). This number likely includes the benefit of e-commerce, larger store sizes, and growth in franchise stores, so annual comp store sales over that time frame likely ran less than 20%, which is significantly worse than what we saw at the much larger Lululemon…

We are currently in the soft launch of a subscription service for dedicated research of the retail and consumer industry. We will slowly transition the bulk of our public coverage to the subscription model over the coming months but will always provide all of our work on Nike and Restoration Hardware free of charge. Currently we have 13 companies under coverage. Please add your email to our normal distribution list for timely notifications of future research. You can find our website at: M Squared Capital.