Nike Distribution Needs A “Personal Genie”

U.S. Retail/Consumer - Nike, Foot Locker, Dick's Sporting Goods, Macy's, Academy Sports, Nordstrom, JD Sports, Lululemon, Adidas, Puma, On

All content on this substack is free.

Distribution is the single largest challenge at Nike today. Many seem to think the only issue is innovation and certainly they can improve in that regard. But while it is likely true that innovation solves most problems (i.e. “hot” product often finds a way to sell itself), a company the size of Nike needs both of those engines to run at full steam. Bulls like to think that all Nike needs to do is launch some innovation and everything returns to normal. But what if their distribution problems are largely structural?

We have taken a deep, data driven review of Nike’s distribution health and how that has evolved over the current decade. The good news is Elliott Hill continues to say the right things towards the need for change, including at a Sell-Side meet & greet at the NYSE last week. The bad news is that his predecessor left him in a highly difficult situation – worse than we originally thought before this review.

Footwear distribution is likely current focal point and certainly seems they made progress in this regard. Nike continues to reduce their reliance on lower quality partners such as Kohl’s and Macy’s even despite recent challenges, which we are constructive on. But by how much can quality partners like Foot Locker and JD Sports, who both are a bit more premium positioned than most other partners, pick up the slack? We came into this analysis under the assumption there are plenty of good partners for Nike to shift back to but increasingly that doesn’t seem to be the case. Makes you really wonder why Nike would ever alienate these few partners to begin with.

We are much more concerned longer-term by the company’s Apparel distribution strategy. Macy’s and Kohl’s remain well entrenched in the top five distribution points, while stronger partners like Dick’s Sporting Goods seem to be ambivalent about the relationship. Ultimately, we believe Nike, who remains the largest Athletic Apparel brand in the world, will need to shift towards physical DTC to address this opportunity. Unfortunately, in a similar manner to most of Nike’s history, the Apparel category appears to remain an afterthought despite the much larger TAM opportunity.

One of the more interesting takeaways for us: seems Nike took ASP’s (specifically list price) up too much relative to consumer acceptance for their product. While may sound obvious given current discounting, puts an emphasis on idea that Nike didn’t learn much about how pricing should only follow innovation a few years back. Does anybody else remember when they had to lower prices on Signature Basketball shoes? Could imply they might need to take list prices back down a bit for some product at a point, at least until they get brand heat rolling in full motion again. This is a bit different than the “Nike was hell bent on making DTC work so gave promos to push that channel” narrative we constantly hear.

We partnered with Flywheel Alternative Data to analyze the relative health of Nike’s distribution footprint. The data set that we used is largely North American and European focused. Our discussion of SKU Index is primarily focused on the relative Nike presence at various retailers and does not imply sales (which is a function of many other factors).

At Nike we have seen a gradual increase in the average list price of both Apparel and Footwear, although certainly more pronounced in Footwear. The percentage of Apparel products on markdown appears relatively flattish with a slightly increasing trend in recent years. The percentage of Footwear products on markdown has clearly been in an uptrend since early 2022 and recently reached levels last seen during the height of COVID. This is significantly different than our recent work on Under Armour, which shows higher trends in list prices accompanied by a lower markdown mix, which you can see in more detail here: “Send In The Cleaners” Under Armour Style.

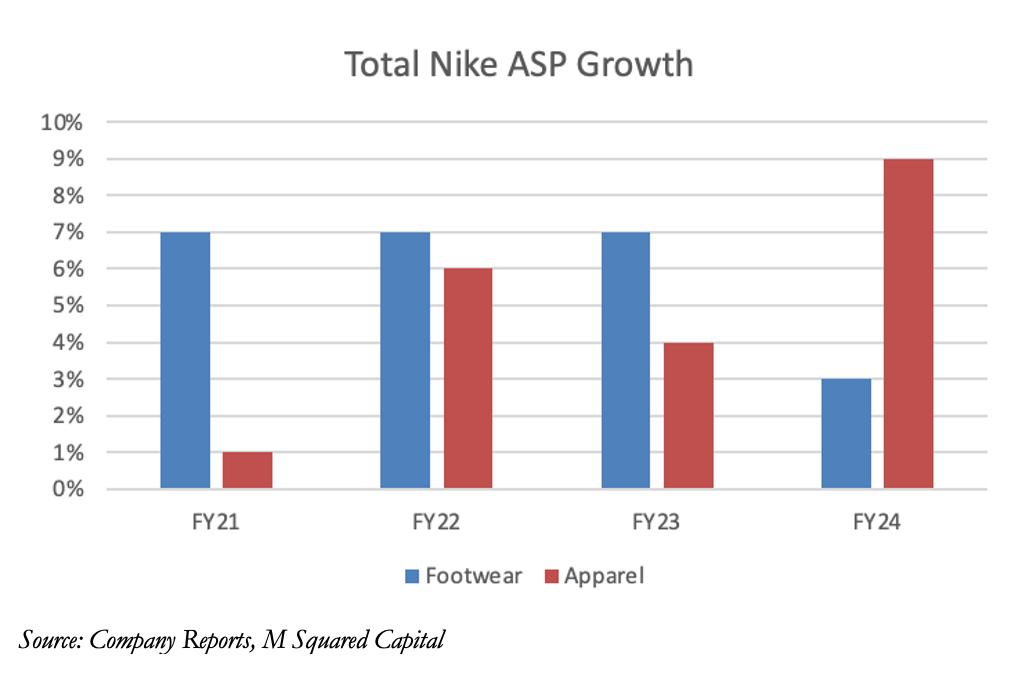

Over this decade, this has translated into approximately 10% growth in terms of out the door pricing in Apparel and around 15% in Footwear. Per the previously linked note, you will notice we have seen substantially better growth at Under Armour in Apparel and something similar in Footwear.

Not hard to reconcile this with Nike’s own reported ASP growth this decade. Reported footwear ASP growth has been slightly higher than apparel. Of course, one of the largest stated reasons for the growth in general has consistently been the shift towards DTC from wholesale, which shows up in Nike’s numbers but should already largely be reflected in the out the door pricing charts above.

DTC

It is widely accepted that Nike transitioned to a push model (using discounts) with its own DTC business over the past few years and that is what most wholesale partners blame for their own challenges with the brand. JD Sports outright called Nike’s DTC promos out during its 3Q conference call in November and in December, Foot Locker noted the pace of promotions in North America DTC was bleeding into wholesale channels.

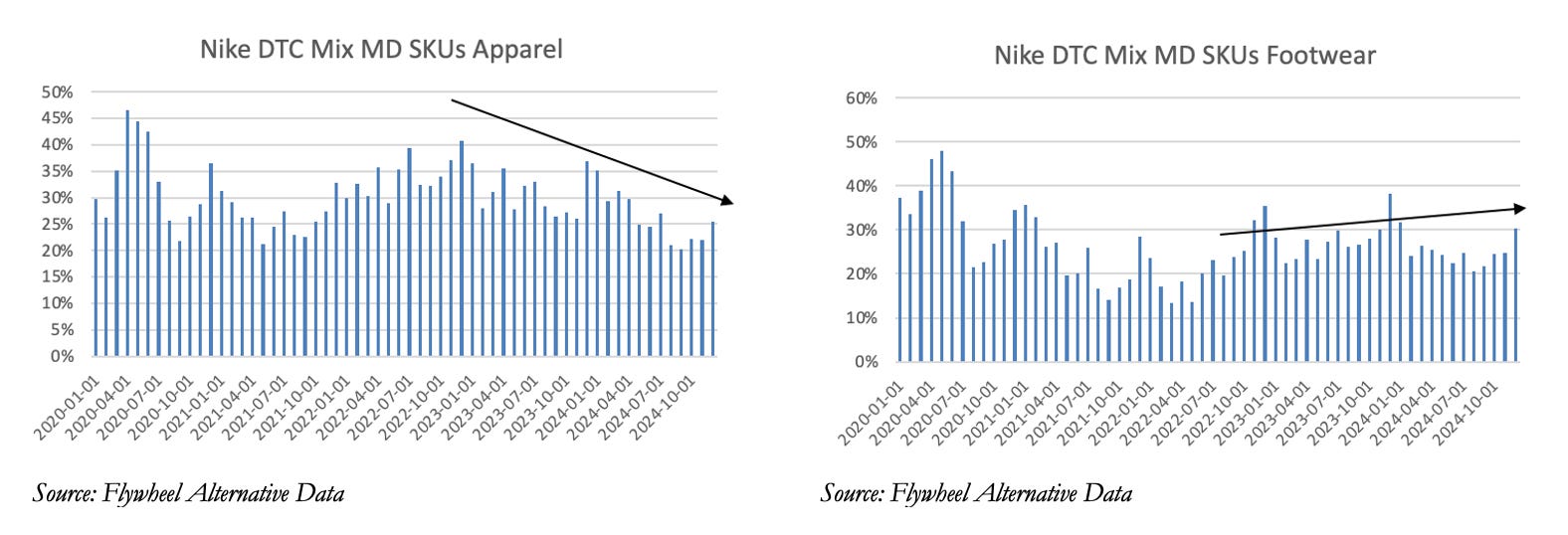

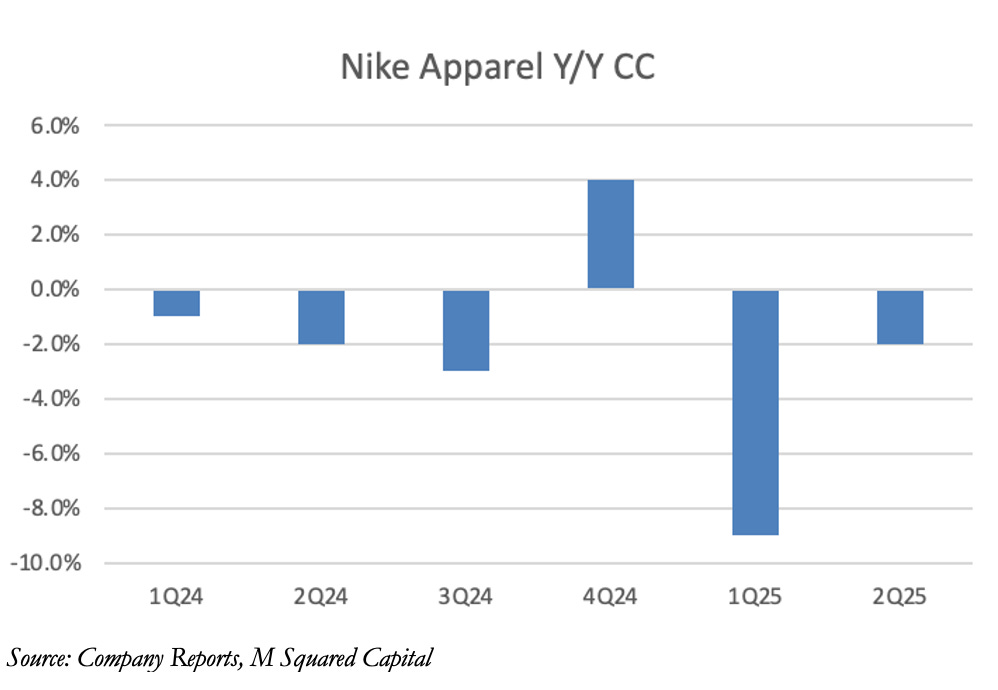

While this may be the case with Footwear, it doesn’t seem to be a fair assessment of the apparel business. We are now sitting slightly above current decade low levels of markdowns relative to the total assortment for Apparel.

And yet this appears mostly as a positive affirmation of how well Nike manages inventory in its apparel business as opposed to any sign of strength. They only had one positive quarter of apparel growth in the last year and half so the business itself has been pressured.

APPAREL

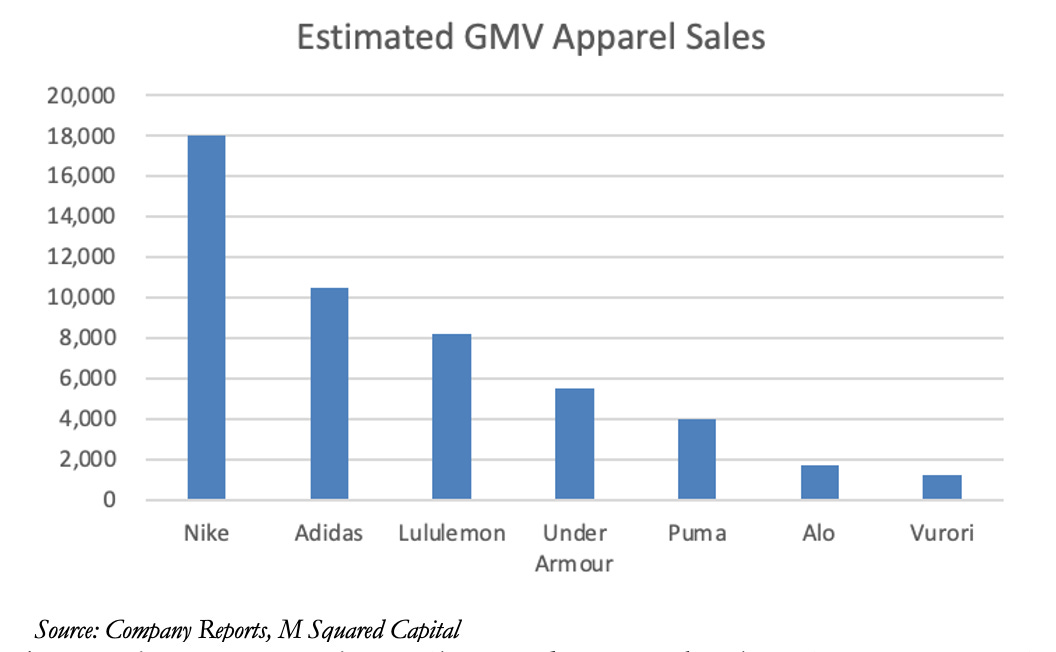

Let’s talk more about Athletic Apparel. Here is how that world looks these days in terms of market share:

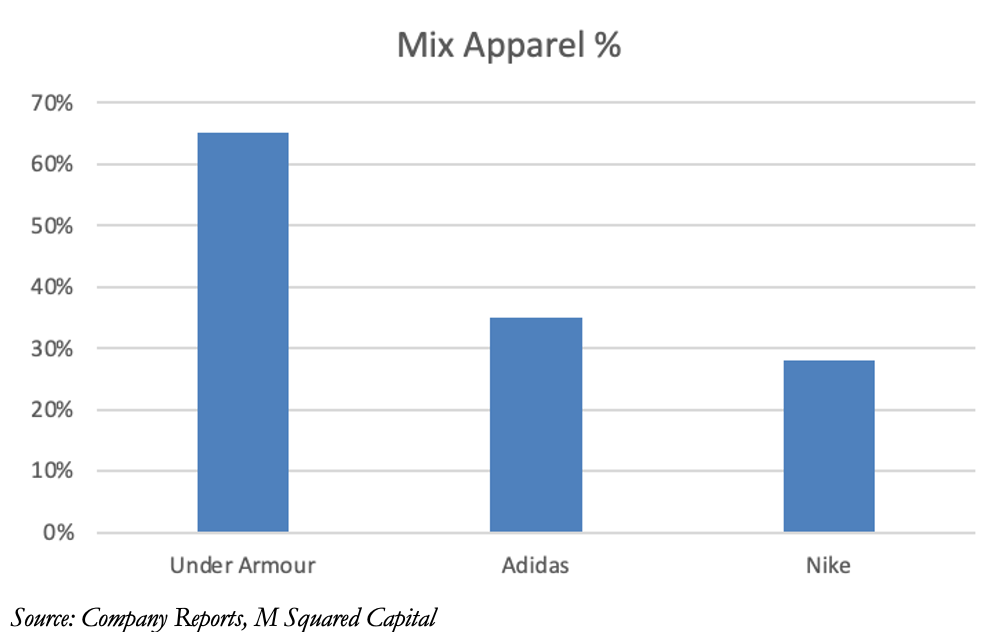

As much as I agree that Nike needs to get back to its roots, starting with Running footwear, Apparel remains the largest opportunity within the Athletic industry today. The total Apparel industry is substantially larger than the total Footwear industry. Yet here is the current mix of Adidas, Nike, and Under Armour:

Point being – the traditional athletic companies (Adidas and Nike) clearly aren’t addressing the bigger opportunity here very successfully. Particularly when you realize that Alo, Lululemon and Vuori are almost entirely apparel driven. I do suspect those names will have a difficult time getting into Footwear though.

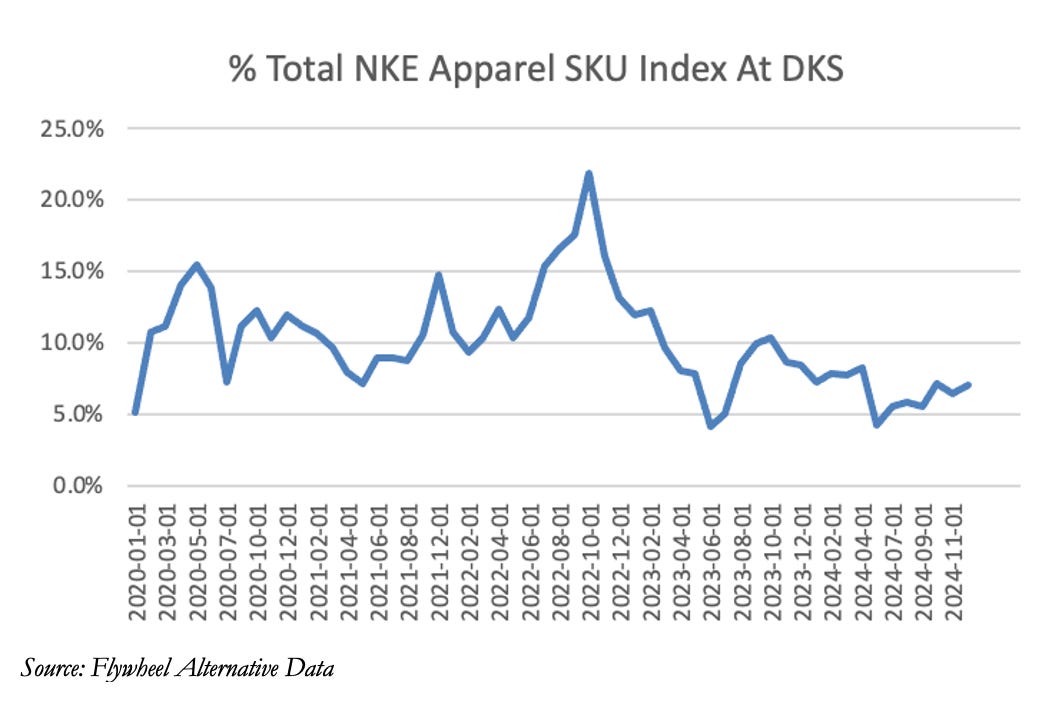

We have written a substantial amount about the limitations of Nike’s current Apparel distribution footprint. After Nike Direct (in the US that is mostly e-commerce combined with factory outlet stores), these are last month’s primary vendors for the company’s Athletic Apparel by overall SKU index (in order): Macy’s, Zalando, Kohl’s, Nordstrom, and Dick’s Sporting Goods.

None of these names scream “growth retail” other than Dick’s Sporting Goods. And funny enough, Dick’s has become less important in the mix over the past several years. It would seem like the only merchants well versed in the Athletic Apparel category have consistently voted “no” on Nike Apparel product for over two years at this point. I wonder if that’s because Nike’s designers are required to make product for what is largely a losing form of distribution while others, who are less restrained, simply try to make good product?

There are many potential reasons for this, such as SKU rationalization efforts or the shift to DTC. But let’s compare the mix of Dick’s in Nike’s distribution footprint to other, maybe less ideal, retailers. Nike appears to need Macy’s today more than at any other point this decade. While it looks like Nike was making progress towards reducing its reliance on Kohl’s, that all reversed mid 2024 and is back to historical levels from earlier in the decade.

We believe that its highly debatable if Nike can easily get back to its dominance and compete in Apparel with “innovation”. Not only is Nike a Footwear first company, Elliott Hill himself has said almost nothing about Apparel and they clearly are pre-occupied trying to figure out why On can out innovate them in Running. And even if they did, how do they solve for the substantial distribution disadvantage? Even On knows this is a problem in Apparel as they specifically mentioned it at the ICR conference this year.

FOOTWEAR

Nike has a vastly different distribution footprint for Footwear than it does for Apparel, but two names are consistent in the top five: Zalando and Dick’s Sporting Goods. Foot Locker and Dick’s Sporting Goods are clearly their most important physical brick & mortar partners, likely followed by JD Sports when you combine with Finish Line. Foot Locker had a higher penetration in the mix than its long-term average, which we found both interesting and encouraging.

For those that care, Academy Sports ranked 16th, DSW 19th, Nordstrom Rack 20th, Macy’s 22nd, and Kohl’s 32nd. Both Kohl’s and Macy’s have dramatically dropped from their longer-term average, which is also encouraging. The long-term trend toward Nike reducing exposure to both retailers appears consistent with efforts to elevate the brand. Although it does appear that Nike, under John Donahoe, went heavy to Kohl’s slightly after they intentionally pulled back from Foot Locker. At least that seems sorted by now.

We have already dug into the ongoing competitive dynamics at Foot Locker in our recent report: Ground Zero in the Athletic Footwear Debate. Continue to strongly believe that Nike’s performance specifically at this partner will be the single best KPI towards any potential turnaround.

FIN